The finance sector has always depended on data organization, interpretation, and governance. And each technological shift, from ledgers and spreadsheets to cloud-native platforms and neobanks, has aimed to make financial decision-making faster, more reliable, and more scalable.

However, when modern financial institutions began to recruit AI for planning and executing tasks with limited human supervision, a more fundamental question emerged:

At which point does automation become autonomy?

In this article, we’ll explore how the finance sector automation has evolved from rule-based to goal-driven, outline the core use cases of AI agents in finance, and see how they impact business development and scalability.

ERP to RPA to ML: evolution of intelligent automation in finance

Since the establishment of the modern banking and finance sector at some point between the XIV and XV centuries, it has always had some form of data governance. At the start, there were records such as goldsmith receipts, bills of exchange, income ledgers, and deposit and loan records, which were later replaced by Excel spreadsheets and pivot tables.

ERPs: enterprise-grade data organization

The first true precursor to modern ERP systems emerged in the 1960s when IBM developed mainframe-based Material Requirements Planning (MRP) systems.

These early systems were not financial tools; they were designed to optimize manufacturing operations by managing production schedules, inventory levels, coordinating procurement, and forecasting material demand.

However, once operational data has been organized, financial data followed. Second-generation MRPs had accounting functions, such as ledger consolidation, cost accounting, and budget tracking, and introduced some critical data governance bits to the financial sector, such as:

- Single source of truth: unified ledgers across geographies

Standardized processes: IFRS/GAAP compliance became enforceable at the system level - Audit trails: automated logging of every financial action

- Real-time reporting: reduced month-end close cycles

Yet, ERPs were fundamentally systems of record, not systems of intelligence. They stored and structured data, but decision-making remained manual.

This limitation set the stage for rule-based automation.

Rule-based automation (RPA)

Robotic process automation is often called the first step in intelligent automation in financial services. It is usually built on top of data governance systems, such as ERPs, and uses bots to automate routine tasks, such as:

- logging into systems

- moving data between systems

- processing invoices

- reconciling accounts

- generating compliance reports.

Using RPA in finance and accounting allowed for boosting efficiency and reducing human errors in processes such as:

- Accounts payable processing. RPA automated invoice capture, three-way matching, exception handling, and payment scheduling, significantly reducing cycle times and manual reconciliation effort.

- Know Your Customer (KYC) and Know Your Business (KYB) verification workflows. Bots collected, cross-validated, and updated customer documentation across internal and external databases, accelerating onboarding while maintaining compliance traceability.

- Fraud rule monitoring. Rule-based scripts continuously scanned transaction streams against predefined risk thresholds, escalating suspicious activity in near real time.

- Regulatory reporting preparation. Banking automation aggregated data from multiple systems, formatted disclosures according to jurisdictional templates, and generated audit-ready compliance reports with minimal human intervention.

However, RPA in finance still had some structural constraints. For example, it couldn’t catch up to interface updates and required strict, rule-based input. Although bots improved efficiency, they could not predict human behavior.

And that’s where the next stage of intelligent automation in finance begins, with the introduction of machine learning.

Predictive AI (Human-in-the-loop)

Unlike rule-driven RPA bots, ML algorithms used historical data to define user patterns, spot irregularities, and predict user behavior. This allowed the creation of a hybrid data governance model: Human-In-the-loop, which works as follows:

- AI generates predictions or flags

- Humans validate, override, or confirm decisions

- Feedback loops retrain the system

Modern banks, such as JPMorgan Chase, have implemented ML algorithms to automate document analysis, reduce legal overhead, and enhance decision-making, enabling them to save over 360,000 hours of legal work per year. This clearly illustrates how the use of AI in finance improves efficiency, reduces costs, and delivers operational excellence and scalability.

See how healthcare companies use AI to automate billing and subscription management, and the advantages it brings, in our guide.

But what if we go a little further and shift from efficient, yet task-based, ML automation to goal prediction and execution with AI?

AI agents (Goal-driven systems)

AI agents in finance are the cutting-edge automation technology: systems capable of multi-step reasoning, tool usage, and autonomous execution toward defined objectives.

These systems have defining features:

- Large Language Models (LLMs): used for providing semantic reasoning capabilities that allow agents to interpret financial policies, process unstructured documents, and translate natural-language objectives into executable workflows.

- Reinforcement learning: enables optimization by continuously adapting decision strategies based on performance feedback and changing market conditions.

- API orchestration: ensures governed data coordination across ERPs, treasury platforms, compliance engines, and external financial infrastructure.

- Autonomous decision trees: assist in creating multi-step execution logic that adjusts system actions in response to real-time financial data and risk thresholds.

How does it work in practice?

For example, you set a business goal:

“Reduce net credit risk exposure in the corporate lending portfolio while preserving target yield thresholds.”

An agentic AI in finance would execute the following processes to achieve this objective:

- Ingest portfolio and retrieve loan-level exposure data, repayment schedules, and internal risk ratings.

- Access current risk distribution, probability of default, and risks across industries, geographies, and rating bonds.

- Detect emerging deterioration signals by analyzing behavioral, macroeconomic, and market indicators.

- Model portfolio performance under adverse scenarios to quantify expected loss shifts.

- Identify optimization levels and actionable interventions (e.g., repricing, credit insurance, collateral restructuring).

- Propose a prioritized execution plan that reduces risk-weighted assets (RWA) and maintains a minimum portfolio yield.

- Cross-check recommendations against internal policy, regulatory capital requirements, and liquidity coverage ratios.

- Initiate governed execution workflows: adjust underwriting criteria, queue loan sale transactions, and prepare credit committee memos.

Overall, the structural evolution of intelligent automation in financial services can be summarised as:

| Era | Core Capability | Limitation |

| ERP | Data centralization | No execution automation |

| RPA | Deterministic task automation | No contextual intelligence |

| ML | Predictive insight | Requires orchestration |

| AI Agents | Goal-driven reasoning | Governance and control complexity |

Core use cases of AI agents in finance

Corporate finance remains one of the most demanding sectors that uses AI automation in business. However, according to McKinsey’s State of AI report, the majority of companies are still in the experimentation or pilot phases of adoption and are not ready to scale.

This can be due to regulatory constraints, model risk governance, auditability requirements, and capital sensitivities that slow adoption. But even at the pilot stage, AI automation can enhance competitive advantage while increasing operational complexity for organizations. So, let’s examine where agentic AI in corporate finance can deliver measurable, controlled business value.

Treasury & liquidity

Treasury and liquidity functions are strong candidates for the use of AI in finance and capital allocation without breaching risk or policy constraints.

- Dynamic cash allocation. AI agents can aggregate real-time balances, forecast inflows and outflows, and reallocate liquidity across entities or instruments within predefined limits, optimizing yield while safeguarding covenant and regulatory compliance.

- FX hedging within policy bands. Agentic AI can recalculate net currency exposure, evaluate the cost of hedging versus risk reduction, and execute or recommend hedging actions when thresholds are breached, while strictly adhering to treasury policy and accounting constraints.

Risk management

As capital requirements tighten and uncertainty increases, agentic systems enable forward-looking exposure control rather than periodic reporting.

- Continuous exposure monitoring. AI agents consolidate credit and market exposures, stress-test portfolios in real time, and flag or recommend adjustments when concentration or capital thresholds approach defined risk appetite limits.

- Real-time anomaly triage. It prioritizes suspicious transactions, gathers contextual data, prepares investigation summaries, and auto-clears low-risk cases within tolerance rules, reducing investigative cycle time and workload.

Compliance

Regulatory frameworks are constantly growing in complexity, and agentic AI solutions for enterprise automation help structure interpretation and documentation under controlled oversight.

- Regulatory mapping

The agent parses new regulations, maps obligations to internal controls, identifies compliance gaps, and maintains a live obligation-control matrix for review and validation. - Automated documentation generation

It compiles draft reports, control narratives, and regulatory disclosures directly from system data, standardizing outputs while preserving human approval checkpoints.

Financial planning and analysis (FP&A)

Strategic agility and efficiency rely heavily on analytical speed, and agentic AI shifts FP&A from static reporting to structured insight generation.

- Autonomous variance analysis. AI agents can decompose actual-versus-plan deviations into core drivers, link them to operational or market factors, and produce concise executive-ready explanations.

- Multi-scenario simulation. It models alternative revenue, cost, and macro assumptions, quantifies impact on cash flow and capital, and ranks scenarios by risk-return profile for decision support.

Explore our latest insights on AI audit software and the value it brings to your business.

Across treasury, risk, compliance, and FP&A, agentic AI reduces cycle times, lowers marginal operating costs, and deepens analytical insight by embedding structured, goal-driven automation.

Ways in which AI agents in finance can accelerate decision autonomy in digital-first environments

Unlike traditional enterprises, the core product of financial institutions is balance sheet management, risk transformation, and information asymmetry arbitrage, all of which depend on precision, timing, and data integrity. That’s why the operating model of financial companies increasingly reflects several foundational characteristics:

- API-native architectures

- Modular infrastructure

- Real-time transaction streams

- Tighter feedback loops

This digital-first foundation lowers the technical barriers to deploying finance AI agents, but let’s explore the specific areas where they make the most impact.

Autonomous credit underwriting

Speed and risk precision directly affect competitiveness in digital lending environments; agentic AI can transform underwriting from static, score-based approval to a streamlined credit management flow.

- Dynamic credit limit adjustment. AI continuously reassesses borrower risk using transactional behavior, income signals, and repayment patterns, adjusting credit limits within predefined capital and policy boundaries without requiring full re-underwriting cycles.

- Risk threshold adaptation within capital constraints. It recalibrates approval thresholds in response to portfolio performance and capital adequacy requirements, ensuring the target growth is met without breaching regulatory or internal risk appetite limits.

- Portfolio-aware pricing models. The banking automation system dynamically prices loans based on expected loss and capital consumption, optimizing yield while maintaining diversification and concentration controls.

Real-time fraud intervention

As transaction velocity increases in digital channels, fraud management must shift from post-event detection to proactive intervention. This can be achieved with:

- Payment authorization agents. The AI agent evaluates transactions in milliseconds using contextual risk signals and behavioral history, approving, declining, or step-up authenticating payments based on dynamic risk scoring.

- Behavioral anomaly detection. Agentic AI continuously models user-specific transaction baselines, identifying deviations in location, device, timing, or spending patterns that indicate elevated fraud probability.

- Automated transaction freezing within risk bands. When risk exceeds defined tolerance levels, the system temporarily restricts accounts or transactions while initiating verification workflows.

Embedded finance optimization

Digital finance ecosystems often use third-party platforms to integrate lending, payments, and liquidity tools and workflows. Here’s how AI agents in finance can optimize embedded finance:

- Merchant settlement timing agents. AI agents dynamically adjust settlement cycles based on liquidity cost, merchant risk profile, and platform cash flow strategy, balancing working capital efficiency with risk exposure.

- Dynamic working capital allocation. Agents can reallocate capital across merchants or segments in real time according to demand, repayment velocity, and risk-adjusted return metrics.

- Adaptive BNPL pricing. The system adjusts buy-now-pay-later pricing and installment terms based on customer behavior, merchant category risk, and fluctuations in funding costs.

AI-driven financial guidance

Fintech platforms are evolving from transactional tools into financial ecosystems, and agentic AI can deliver personalized, goal-oriented financial management at scale.

- Autonomous financial health calibration. The agent analyzes income, spending, and debt structure to deliver timely, behaviorally informed recommendations that improve repayment discipline and financial resilience.

- Dynamic savings reallocation. It automatically redistributes surplus balances across savings goals, yield products, or debt reduction pathways based on changing cash flow patterns.

- Personalized credit management. The system proactively suggests refinancing, credit utilization adjustments, or changes to the repayment schedule, aligned with both borrower stability and lender risk objectives.

Overall, AI agents in banking can enable fintech firms to achieve higher approval rates without proportional increases in risk, improve loss ratios through earlier and more precise intervention, and shift toward proactive customer engagement that strengthens retention while optimizing portfolio performance.

The business case for autonomy: how to get ROI from agentic AI in finance?

Now, let’s look at how you can measure the efficiency of AI use in finance and quantify ROI from your agentic AI initiatives. To do this, let’s focus on four measurable value pillars that directly influence margin, risk profile, and strategic capacity.

Efficiency gains

The most immediate ROI from agentic AI in finance comes from measurable reductions in operating cost per transaction and compression of end-to-end process cycle times.

Unlike basic automation, autonomous systems not only reduce manual workload but also exception handling, rework, and supervisory overhead.

Deloitte’s Global Intelligent Automation Survey reports that organizations scaling intelligent automation achieved an average 31% cost reduction, with similar savings projected as programs mature, indicating a durable margin impact rather than a one-off optimization.

In finance functions specifically, IBM Institute for Business Value research links AI deployment to at least a 25% reduction in monthly close cycle time, directly translating into working capital efficiency, reduced earnings volatility, and lower write-offs and forecast errors.

Decision velocity

Latency has a quantifiable cost in financial environments. Delayed credit decisions reduce conversion, slow treasury responses increase liquidity drag, and prolonged anomaly reviews elevate exposure.

The ROI of agentic AI in finance materializes when systems are integrated into existing ERPs, core banking platforms, and risk engines via governed APIs that enable decision-making within operational workflows rather than outside them.

The same Deloitte survey identifies integration complexity as one of the primary barriers to scaling automation, implying that ROI is maximized when AI is embedded directly into transaction flows. Faster decision turnaround times, higher straight-through processing rates, and reduced abandonment rates create compounding revenue and efficiency gains rather than incremental productivity improvements.

Continuous risk mitigation

Risk management tops the list of AI uses with the most transformative results, according to the BCG’s Center of CFO Excellence survey of 280 finance executives. It generates ROI through avoided losses, improved capital allocation, and reduced operational volatility.

A measurable benchmark comes from the U.S. Department of the Treasury (FY2024), which reported that enhanced AI-driven fraud detection processes prevented and recovered over $4 billion in fraud and improper payments, up from $652.7 million in FY2023.

While public-sector payments differ from commercial banking rails, continuous AI-enabled monitoring with faster detection and containment is transferable to financial institutions seeking lower fraud loss ratios and reduced false-positive costs.

Strategic capacity expansion

Finally, the decision autonomy expands analytical and operational capabilities without proportional headcount growth. Agentic systems allow finance teams to process higher transaction volumes, run more scenarios per planning cycle, and evaluate risk and pricing decisions with greater granularity.

Moreover, AI-enabled finance functions reduce forecast errors and improve performance visibility, indicating that automation enhances analytical depth and processing speed. The ROI here manifests in more precise pricing, improved loss ratios, better capital deployment, and the reallocation of human capacity toward higher-value strategic work. effectively increasing enterprise output without linear cost expansion.

The “control vs delegation” dilemma for AI in business automation

The central tension in deploying AI agents in finance lies in governance: how much decision authority can be delegated without compromising control, auditability, and regulatory accountability?

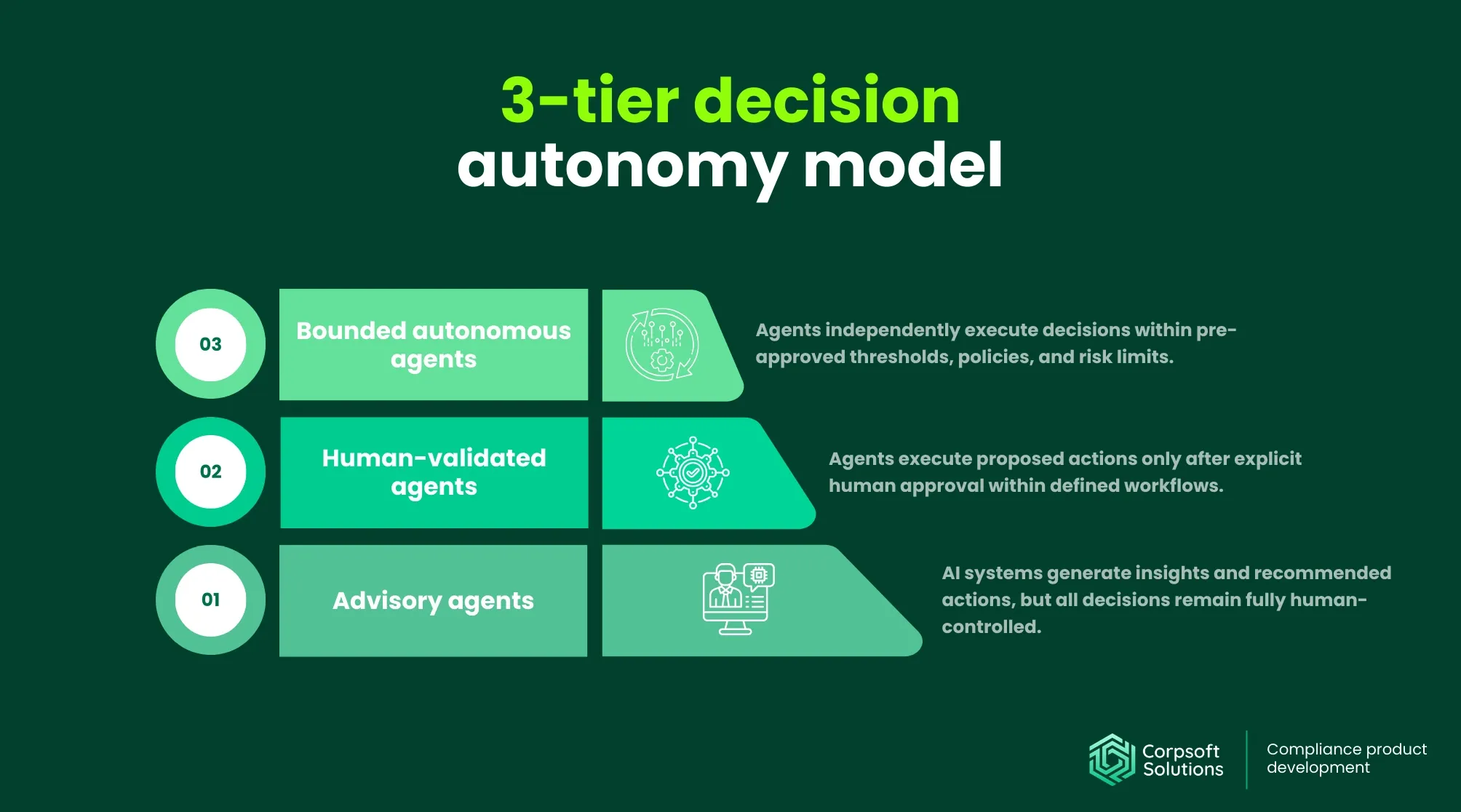

Resolving this requires a structured autonomy framework that aligns delegation with risk tolerance, capital sensitivity, and operational criticality. The 3-tier autonomy model will help you identify areas in which AI agents can operate autonomously and where validation or strict boundaries are needed.

- Tier 1: Advisory agents. These systems generate recommendations, simulations, risk assessments, or draft actions but do not execute decisions; humans retain full approval authority, making the AI a decision-support accelerator rather than a decision-maker.

- Tier 2: Human-validated agents. These agents can initiate actions or workflow steps, but execution requires human confirmation, introducing a structured human-in-the-loop layer that serves as an additional safety control for high-impact financial decisions.

- Tier 3: Bounded autonomous agents. These systems execute decisions independently within predefined policy limits, capital thresholds, and risk tolerances, with full audit logging and automatic escalation mechanisms when constraints are approached or breached.

How does this impact organizational structures?

As decision autonomy increases, the organization should undergo structural changes to support supervision, control design, and model governance. This requires shifting roles to maintain clearer accountability frameworks around machine-augmented decision systems

| Traditional Structure | Autonomous Structure | Business Implication |

| Transaction-heavy processing teams | Fewer transactional processors | Reduced manual throughput roles as agents handle reconciliations, monitoring, and routine decision-making |

| Operational supervisors | More oversight of architects | Increased demand for professionals who design control frameworks, escalation logic, and policy boundaries for AI systems |

| Isolated compliance reviewers | Rise of model risk governance roles | Formalization of model validation, performance monitoring, bias detection, and regulatory documentation functions |

Additionally, the organizational shift unlocks the demand for new skills and capabilities within teams, such as:

- Model literacy. Managers and analysts must understand probabilistic outputs, model limitations, drift risk, and performance metrics to effectively supervise AI decisions.

- Policy design. Organizations must translate risk appetite and governance requirements into executable rules, thresholds, and autonomy boundaries.

- AI lifecycle management. Continuous monitoring, retraining governance, audit logging, version control, and incident response become core operational competencies.

Incremental deployment of agentic AI in finance as a way to minimize implementation barriers

AI transformation programs often fail because organizational, regulatory, and infrastructure constraints are underestimated. A phased deployment model reduces execution risk, preserves control, and allows measurable ROI validation before broader autonomy is granted.

Here’s how it can solve the most common challenges related to intelligent automation in financial services

| Problem | Solution |

| Data fragmentation: Financial institutions typically operate across siloed ERPs, core banking platforms, treasury systems, and shadow spreadsheets, creating inconsistent data lineage and reconciliation gaps. | Incremental deployment allows agents to be introduced within a single, well-defined workflow, forcing structured data mapping and governance improvements in a contained scope before enterprise-wide integration. |

| Legacy infrastructure: Core finance systems often run on legacy architectures not designed for real-time AI orchestration. | A phased rollout enables API layers and middleware connectors to be implemented progressively, reducing operational disruption and validating interoperability before scaling autonomy across critical systems. |

| Regulatory uncertainty: Supervisory expectations around AI governance, explainability, and model risk continue to evolve. | Deploying Tier 1 or Tier 2 agents first (advisory or human-validated) allows institutions to document controls, audit trails, and validation frameworks early, creating regulatory confidence before advancing toward bounded autonomy. |

| Model reliability limitations: AI systems are probabilistic and subject to drift, bias, and performance degradation over time. | Incremental implementation enables controlled performance benchmarking, stress testing, and retraining governance within narrow use cases, ensuring that stability thresholds are met before expanding decision authority. |

| Organizational risk aversion: Finance leaders often resist autonomy due to perceived ambiguity in accountability and concerns about capital exposure. | A staged approach provides visible quick wins and builds internal trust and stakeholder alignment while maintaining explicit human oversight during early phases. |

Conclusion

The success in achieving decision autonomy for financial institutions lies in precisely defining its boundaries, deploying AI incrementally, and anchoring every layer of automation in robust data governance. Autonomy must be calibrated to risk appetite and regulatory exposure with clear escalation protocols, auditability, and model lifecycle oversight embedded from the outset.

As your trusted technology partner, Corpsoft Solutions supports this transition end-to-end: from data foundation design and policy-bound autonomy frameworks to system integration, model governance, and lifecycle management. We focus on building control-grade AI infrastructure that aligns innovation with regulatory resilience, ensuring that autonomy scales without compromising accountability, performance, or trust.

Share this post: